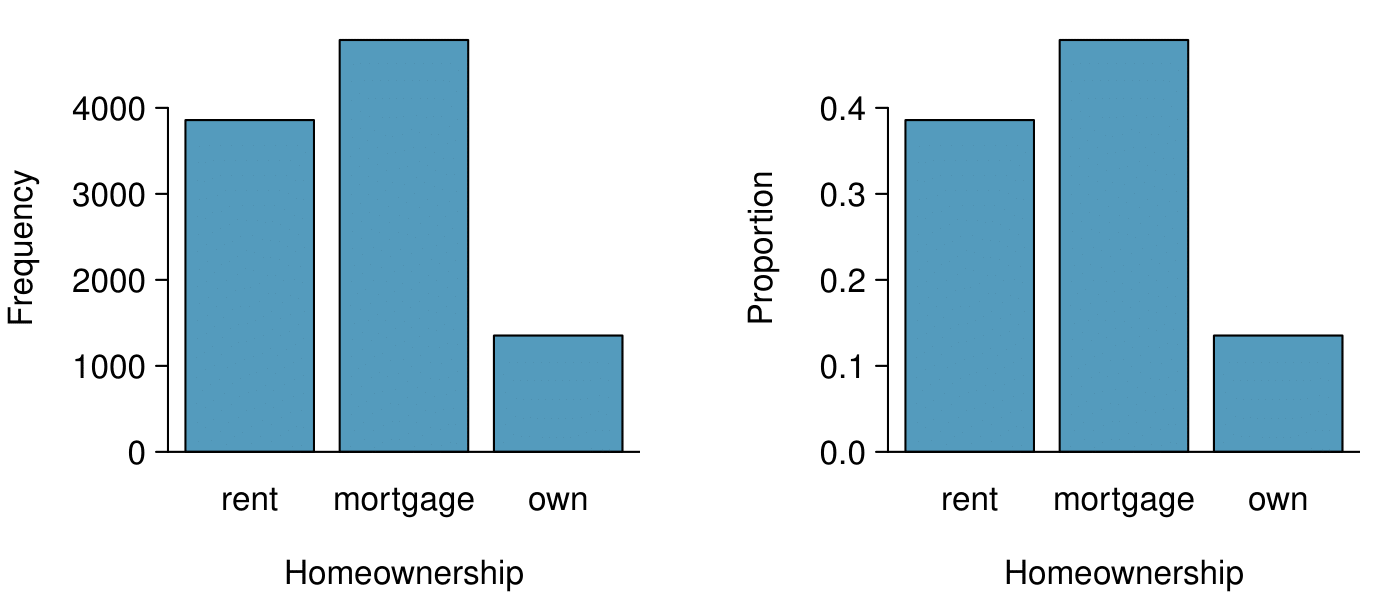

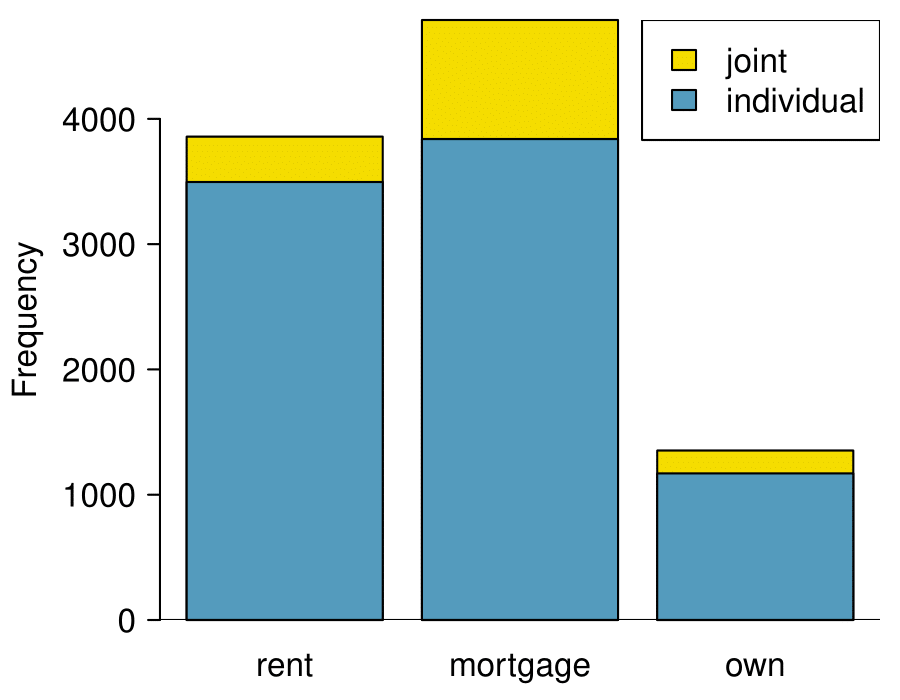

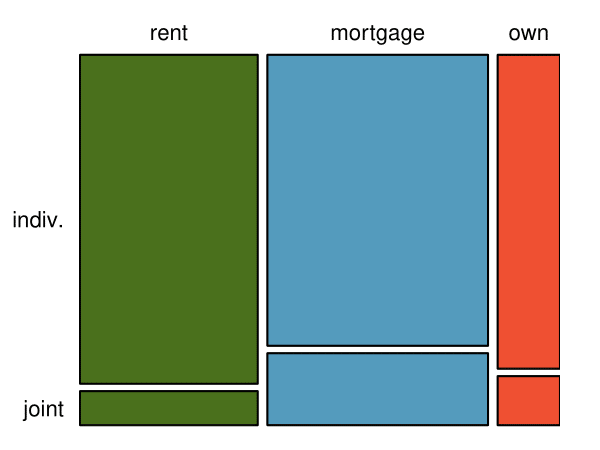

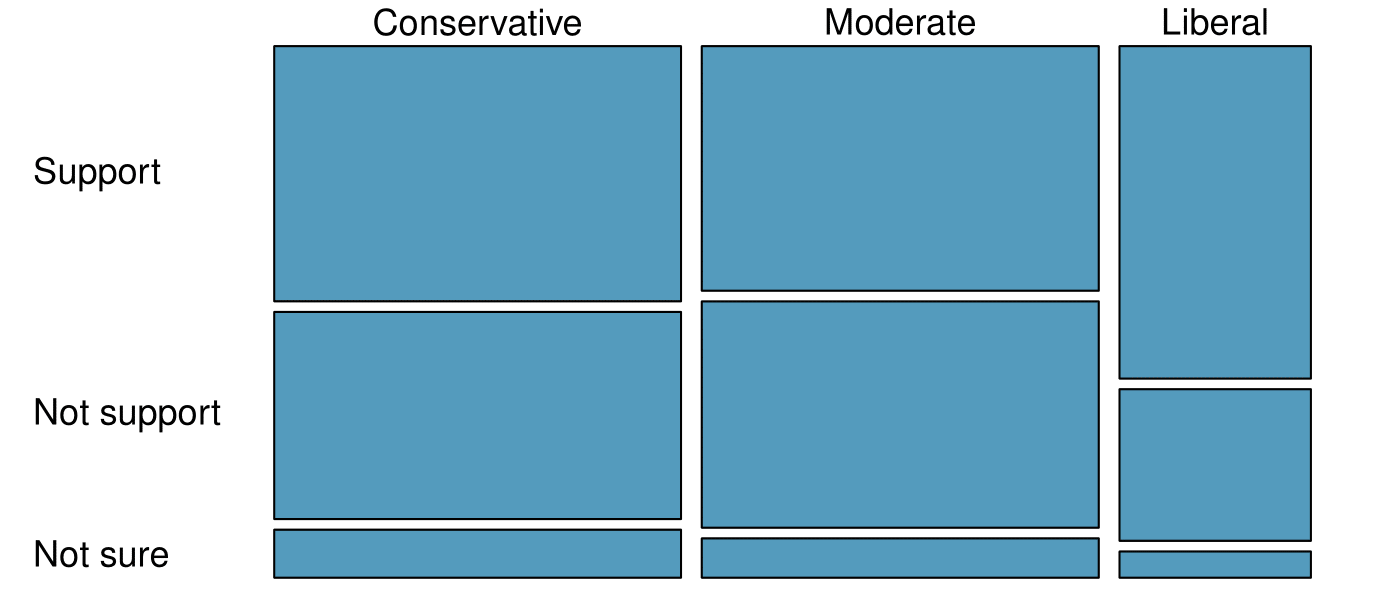

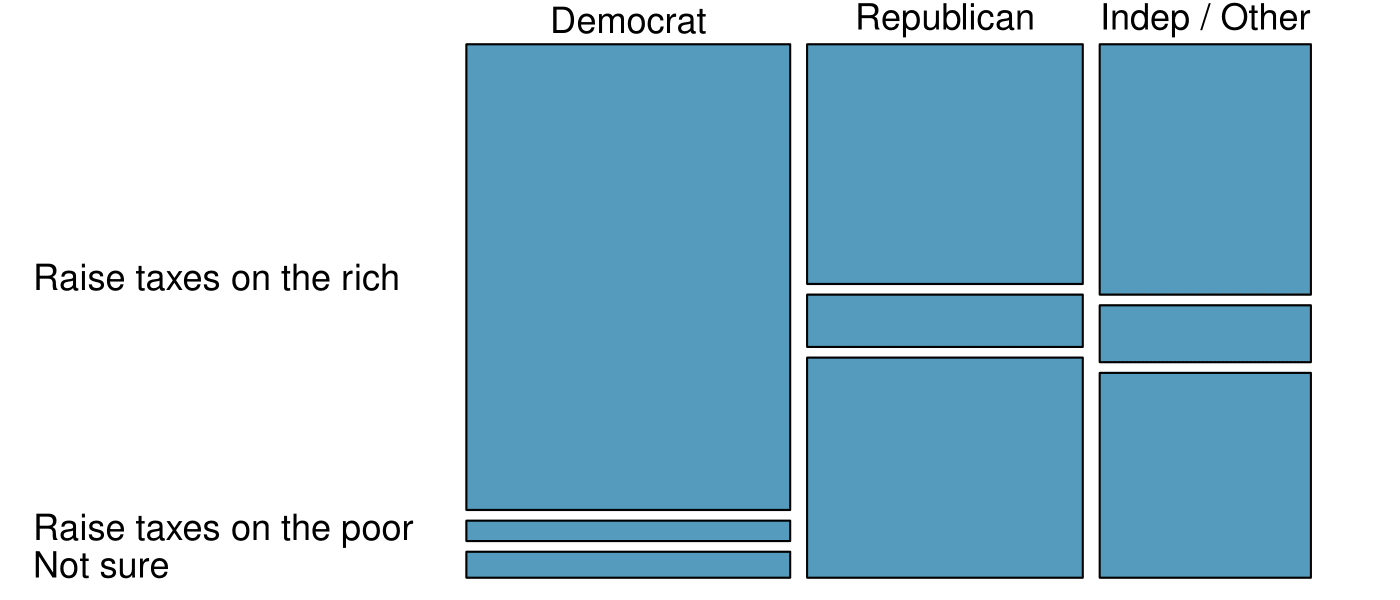

The segmented bar chart is most useful when it’s reasonable to assign one variable as the explanatory variable and the other variable as the response, since we are effectively grouping by one variable first and then breaking it down by the others.

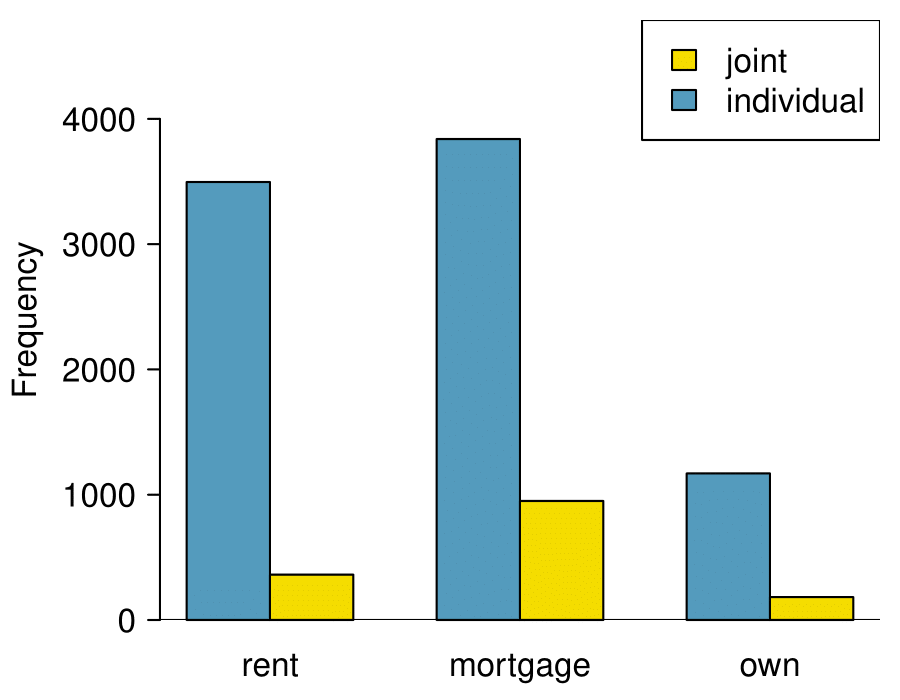

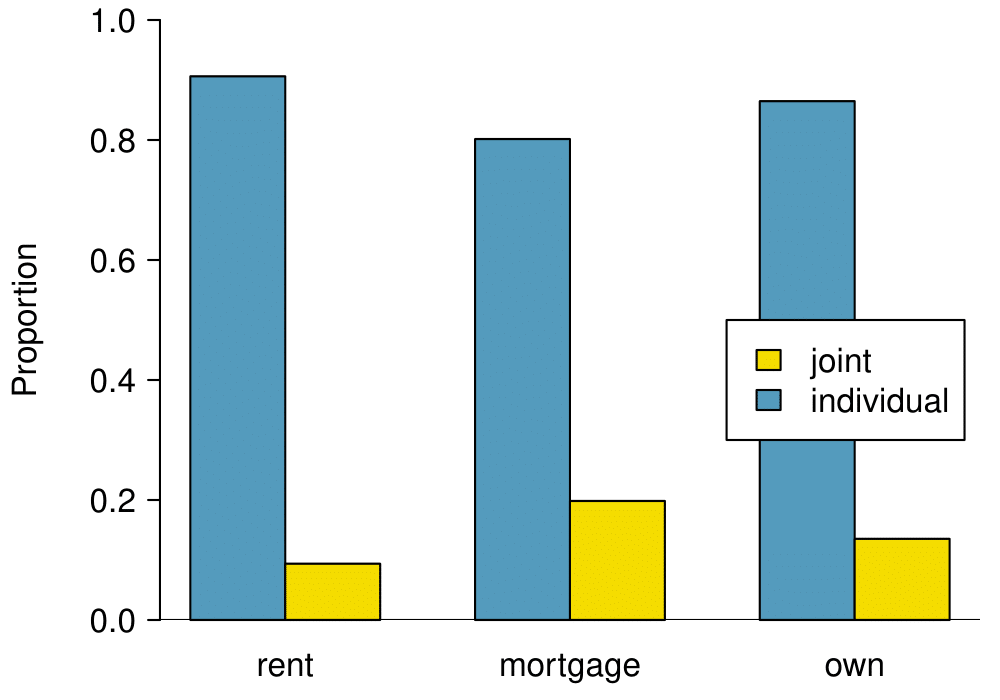

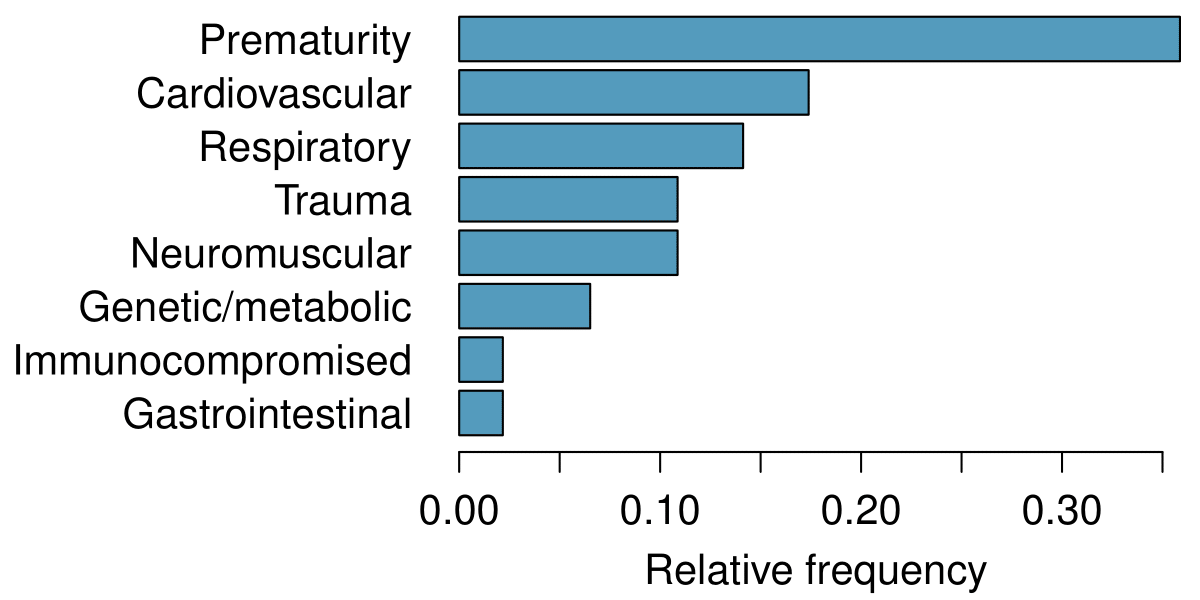

Side-by-side bar charts are more agnostic in their display about which variable, if any, represents the explanatory and which the response variable. It is also easy to discern the number of cases in of the six different group combinations. However, one downside is that it tends to require more horizontal space; the narrowness of

Figure 2.4.11(b) makes the plot feel a bit cramped. Additionally, when two groups are of very different sizes, as we see in the

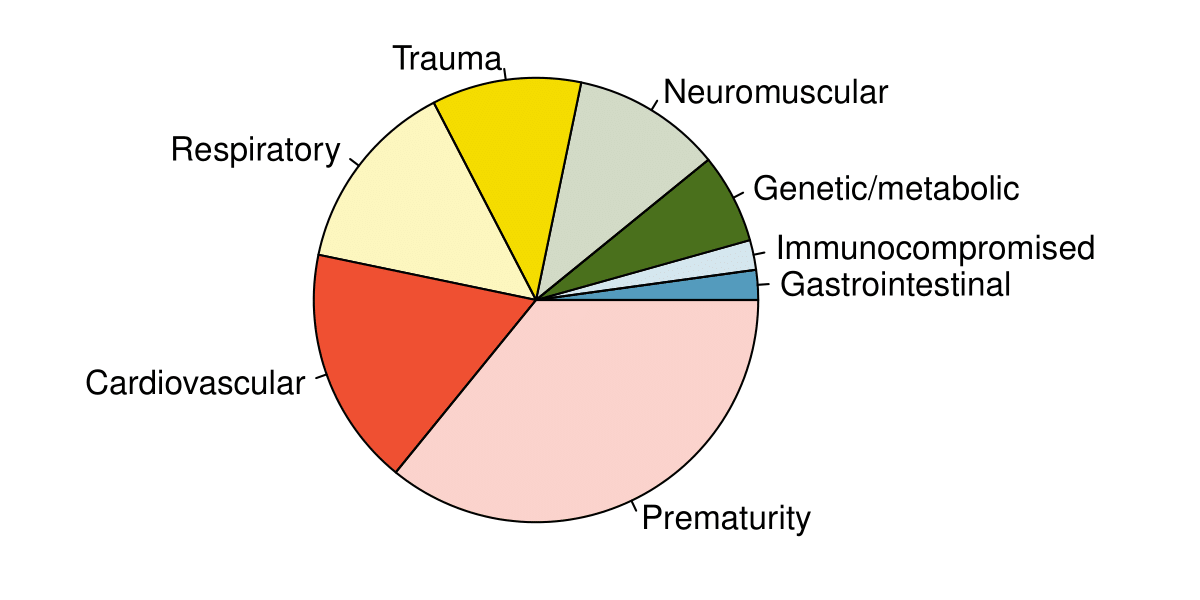

own group relative to either of the other two groups, it is difficult to discern if there is an association between the variables.

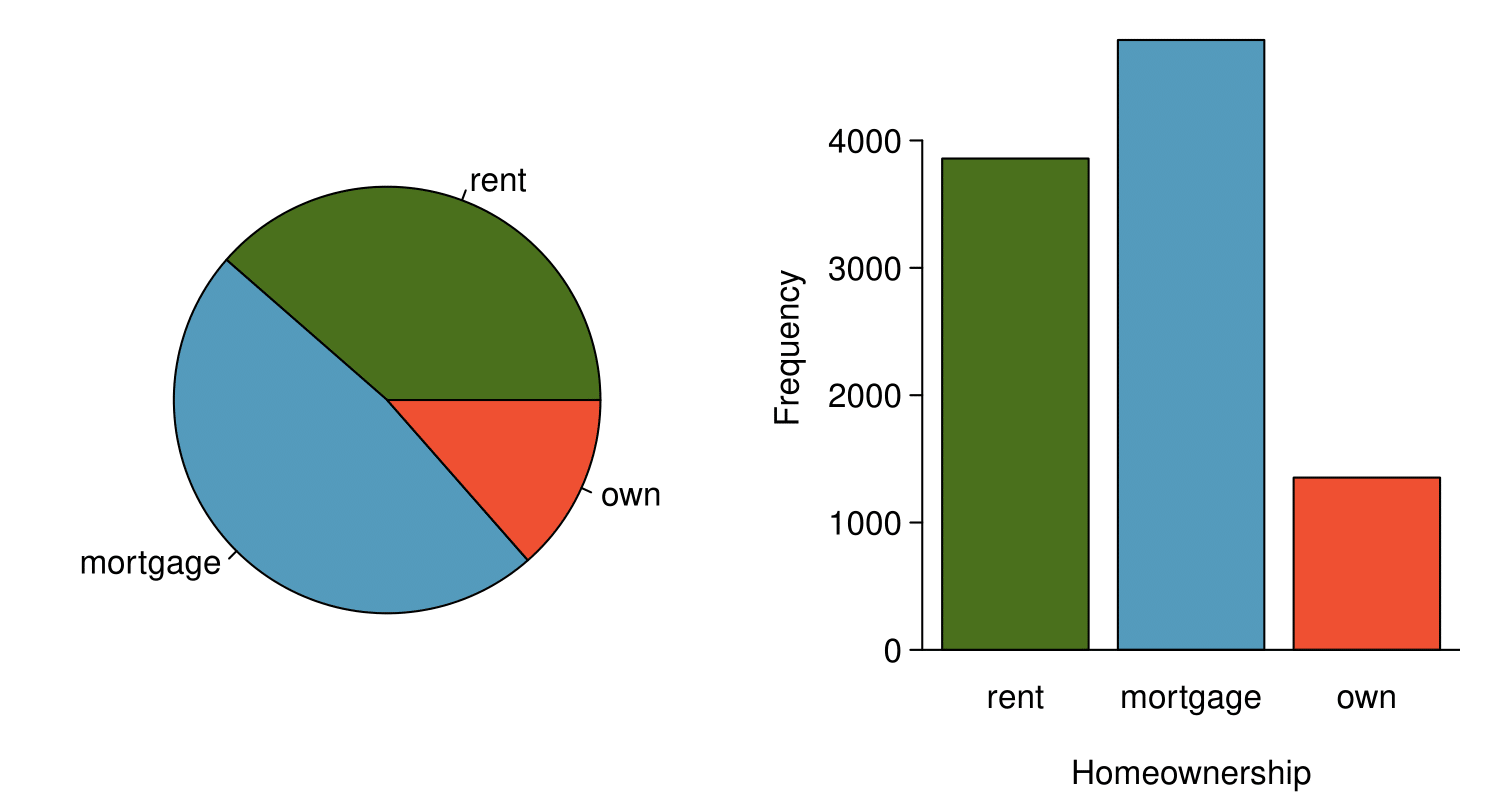

The standardized segmented bar chart is helpful if the primary variable in the segmented bar chart is relatively imbalanced, e.g. the

own category has only a third of the observations in the

mortgage category, making the simple segmented bar chart less useful for checking for an association. The major downside of the standardized version is that we lose all sense of how many cases each of the bars represents.

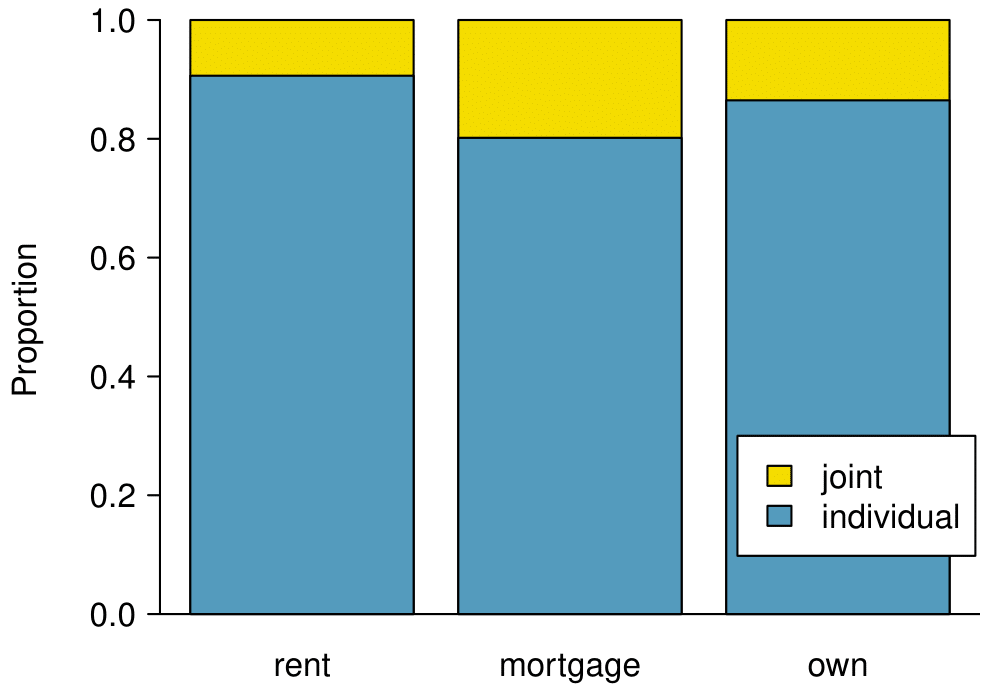

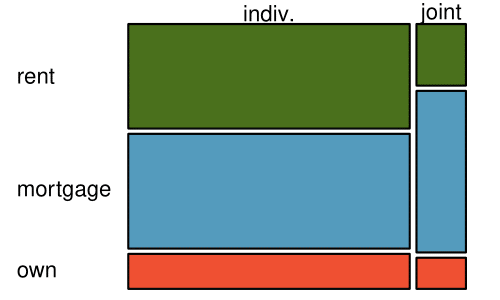

The last plot is a standardized side-by-side bar chart. It shows the joint and individual groups as proportions within each level of homeownership, and it offers similar benefits and tradeoffs to the standardized version of the stacked bar plot.